Smaller contractors generally have a limited understanding of how classifying workers as either employees or subcontractors affect the various types of insurance. This simple distinction can land you in proverbial quicksand and before you know it your overhead.

This article will only deal with the insurance differences between the treatment of employees versus subcontractors or 1099 parties (hereinafter referred to as Subs). I am also going to make the assumption that the reader knows the basics of General Liability Insurance and Workers Compensation and will not go into the basics of these types of insurance.

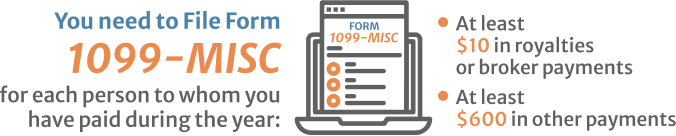

The information about who is an employee and who is 1099 for tax purpose is relatively straightforward and can be found at IRS INFORMATION on 1099.

The two types of insurance that are most affected by the employee vs Sub distinction are workers compensation insurance and General Liability Insurance. When you talk to your insurance agent when you are obtaining your first policy or renewing your current policy you will be asked a few basic questions. The most important of these are:

- The type of work you do.

- Your annual sales.

- Annual Payroll.

- Amount of work subcontracted.

You will be given a premium based on this information provided.

What some smaller contractors fail to understand is that he figures that they have given will be audited at the end of the year and sometimes up to quarterly for WC policies. These Audits have been known to swallow up like quicksand the unsuspecting contractor. I will attempt to set out the nature of these perils below and also give simple tips on how to avoid them.

Workers’ Compensation Insurance Audit

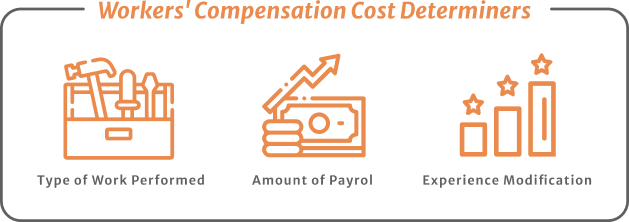

Workers Compensation Insurance (WC) has three basic components in determining its cost.

- First is the type of work being performed. This is based on the riskiness of the profession. A rate for an employee that is an interior carpenter will be significantly lower than an employee that is classified as a roofer. This is just plain common sense. A roofers job is more hazardous as the injuries falling from a height more severe.

- Second, is the amount of payroll. This is where the quicksand finds you. If you classify a worker as a Sub and you do not collect certificates of insurance from these Subs, you will be required to include the amounts you paid them in your payroll when the WC audit is performed. So as an example lets say you paid a roofing subcontractor $100,000 and you did not get a certificate of insurance naming you as an additional insured showing that they had WC coverage. That $100,000 would be included in your payroll at the roofer’s rate and it would not be surprising if you received a bill for $50,000 for this additional payroll.

- Third, is called an experience modification. This is a number that they multiply premium by. It is based on the length of coverage and claims history. In a nutshell, if you have a long history with low claims your multiplier will be less than 1 giving you a lower premium. Conversely, if you have a large number of claims you will have a number greater than 1 and therefore pay more in premium.

General Liability Insurance Audit

A general liability insurance audit is different than a WC. It typically occurs at the end of the policy period. The Insurance Company examines your payroll records and income statements to determine whether the information stated on your application for general liability insurance is consistent with the actual numbers. The three major factors they look at when conducting the audit are set forth below.

- First, they will compare the actual Gross sales of the business to what the figures that were stated on the application. Gross sales include, but are not limited to, total amounts charged for all goods and products sold and services performed. If the sales figure is higher than what is reported on the application you will owe more money. This makes sense as more work you do the greater the risk something will go wrong. These, however, is not so bad if you are aware of the fact that you will owe more money. For example, if you had a Million Dollars more in sales you should have a significantly larger profit. Since you read this article you will have included the cost of insurance in all your projects anyway. The problem is you are unaware of this you can get blindsided by a large audit bill.

- Second, they will audit the type of work you do. If you said that you did mainly interior painting and 75% of your revenue came from roofing you will get a bill. If the nature of your business changes during the year you should talk to your agent concerning these changes.

- Third, they will audit the amounts that you paid to subcontractors. They will compare the amounts paid to subcontractors to the certificates you collected. If these certificates matchup, you have no problem. If it turns out you did not collect certificates from all the subcontractors those Subs will be treated as uninsured. Once this happens you will have to pay the cost of providing the insurance. If you have people working for you and you 1099 them they will be treated as uninsured subs unless you collect certificates of insurance for them. This is how small contractors get in trouble. They do not want the expense of employees so they try to game the system and try to classify real payroll as 1099 payments.

In all almost all instances these above traps can be avoided. The simple solution is to make sure that every single subcontractor provides you a certificate of insurance before they start work. I am sure that every time you have ever worked for a large contractor they have required you to provide them a certificate of insurance naming them as additional insured. You need to be as diligent as the “Big Guys” in collecting these certificates, otherwise, you will become mired in the quicksand that arises from a failure to obtain the certificates. Further, make sure the classification of payee’s as W2 or 1099 payment is consistent with IRS guidelines.

Farmer Brown Insurance Agency

If you need somebody to throw you a rope to get you out of the quicksand or you want to be proactive and avoid any of these traps feel free to reach out to me. I have over 20 years experience in helping small contractors and am the owner of one of the largest internet providers of all types of insurance for contractors on the internet.

![]()

We are experts in General Liability and Worker’s Compensation insurance for contractors, let our experts guide you through this process and keep your peace of mind.